Overseas Education Loans: Your Comprehensive Guide to Funding International Studies

Pursuing higher education abroad is a life-changing decision, but it often comes with significant financial challenges. Education loans for overseas studies can bridge this gap, ensuring that financial limitations do not stand in the way of your international dreams. This guide explains everything you need to know about education loans for studying abroad, their types, eligibility, benefits, and the application process.

Types of Education Loan Providers

Nationalized Banks

Lower interest rates compared to private banks

Income tax benefits under Section 80E

Concessions for students admitted to top global universities

0.50% extra concession for female students

Highly accepted by visa officers

Require extensive documentation

Private Banks

Secured and unsecured loan options

No collateral loans available for Master’s programs

Special rates for premier universities

Faster processing compared to public banks

Higher loan amounts

Non-Banking Financial Companies (NBFCs)

Non-collateral loans up to ₹35–45 lakhs

100% financing coverage including tuition, living, and travel

Pre-admission and pre-visa loans available

Minimal EMI until graduation

Option for top-up loans

International Lenders (available mostly for USA & Canada students)

No collateral or co-signer required

Funding for students in 350 pre-approved universities

Scholarships guidance available

Student’s credit history not necessary

Secured vs Unsecured Loans

Secured Loans (With Collateral)

-> Require property/assets as collateral security

-> Lower interest rates (from 9% onwards)

-> Higher loan limit (up to ₹1.5 crore)

Unsecured Loans (Without Collateral)

-> No assets needed

-> Higher interest rates (11–12% onwards)

-> Limited loan amounts (₹45–50 lakhs)

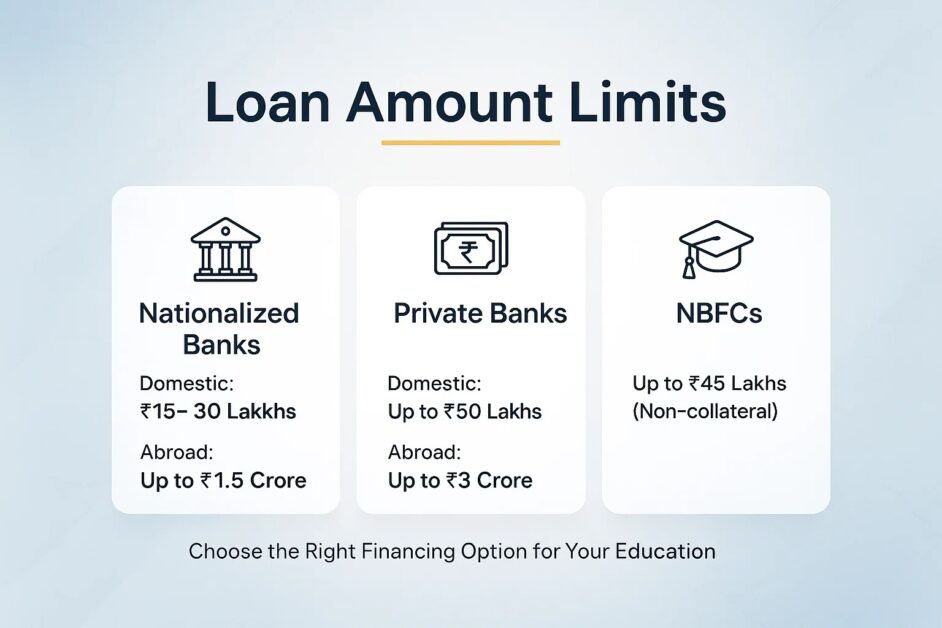

Loan Amount Limits

Nationalized Banks: Domestic up to ₹15–30 lakhs; Abroad up to ₹1.5 crore

Private Banks: Loan amounts up to ₹50 lakh for domestic education and up to ₹3 crore for studies abroad.

NBFCs: Up to ₹45 lakhs (non-collateral)

General Eligibility Criteria

Indian citizenship of applicant and co-applicant

Admission to a recognized foreign university

Minimum 60% academic record in higher secondary or graduation

Co-applicant with credit score above 600

Co-applicant monthly income >₹35,000

Course must fall under approved list of programs

Documents Required

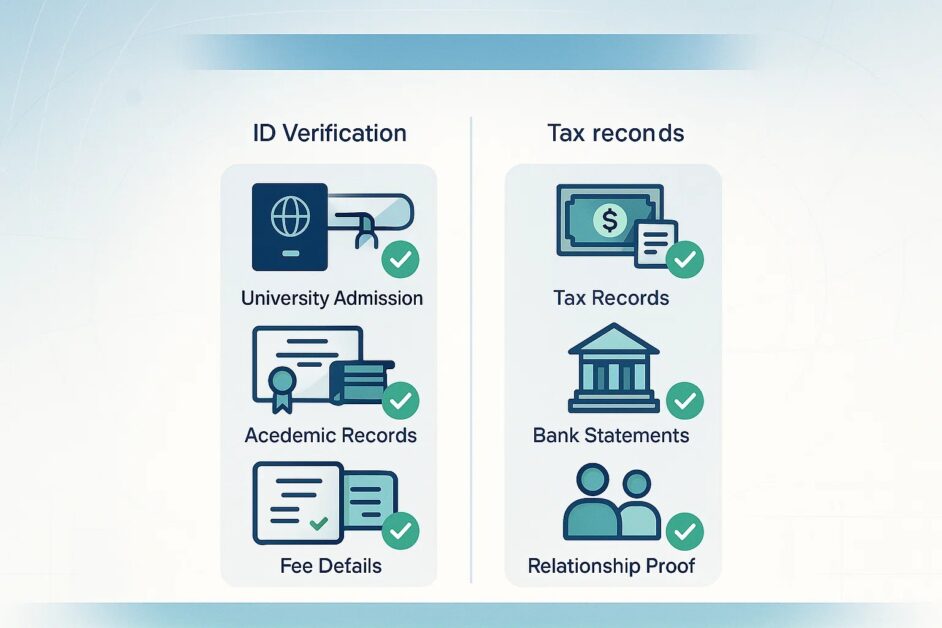

For Students: Required documents include KYC (Aadhaar, PAN, or Passport), admission letter, academic transcripts, and fee details.

For Co-Applicant: Required documents include income proof (salary slips, ITRs, Form 16), bank statements, and proof of relationship.

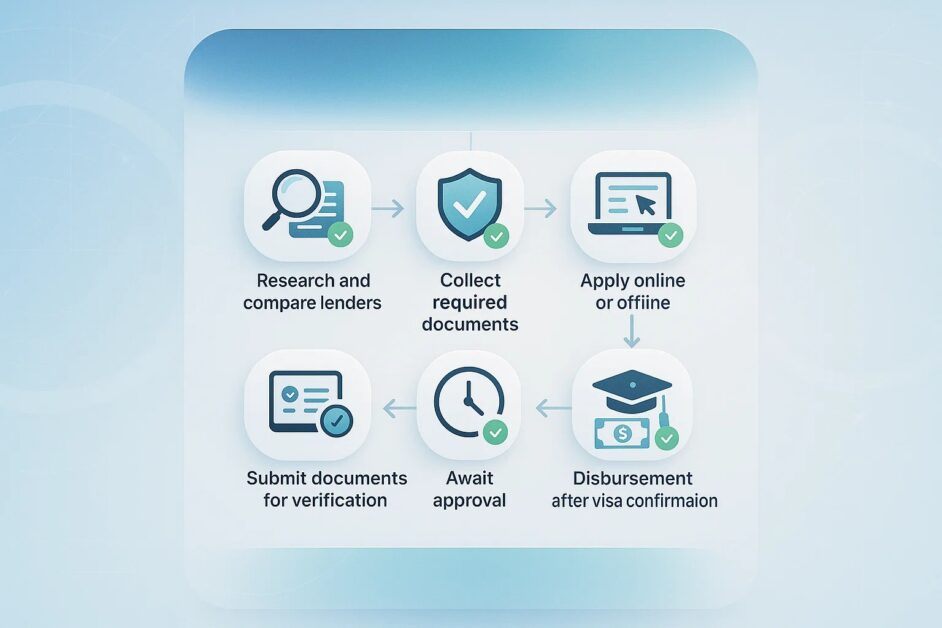

Application Process (Step-by-Step)

Research and compare lenders

Check eligibility criteria

Collect required documents

Apply online or offline

Submit documents for verification

Await approval (7 to 30 days)

Disbursement after visa confirmation

Interest Rates Overview

Nationalized Banks: 9% secured; 10–11% unsecured

Private Banks: 10–11% secured; 11–13% unsecured

NBFCs: 12–15% onwards

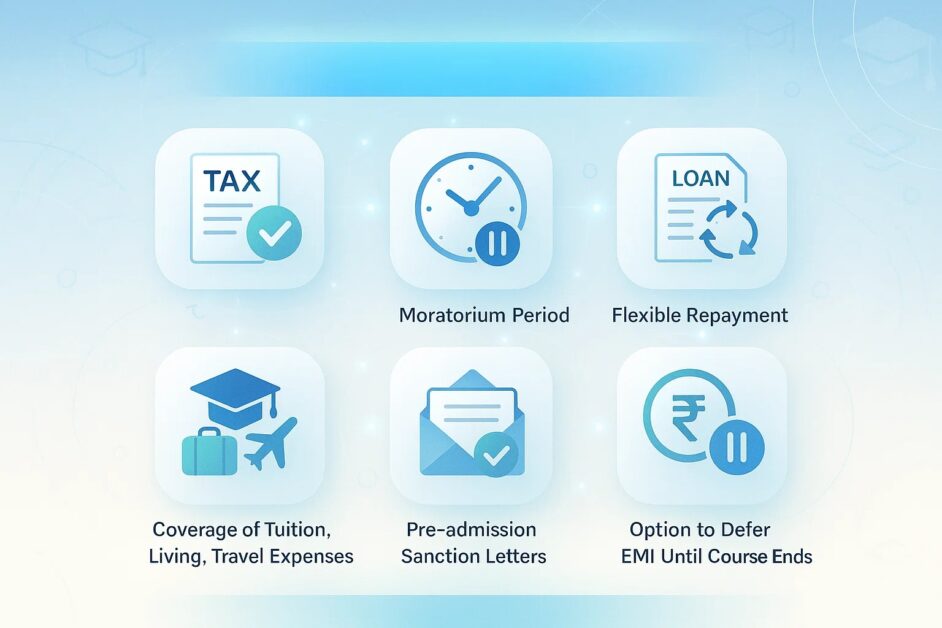

Benefits of Education Loans

Income Tax benefit under Section 80E

Moratorium period of 6 months to 1 year after course completion

Flexible repayment tenure up to 15 years

Coverage of tuition, living, and travel expenses

Pre-admission sanction letters available

Option to defer EMI until course ends

Tips for a Successful Loan Application

Start the process at least 6–12 months in advance

Maintain excellent academic records

Ensure co-applicant’s good credit score

Compare multiple lenders for best rates

Keep documents well-organized

Choose universities from approved lender lists

Consider collateral-free options for flexibility

Conclusion

Financing overseas education is easier today with multiple loan options available through nationalized banks, private lenders, NBFCs, and international organizations. By starting your planning early, keeping finances and documentation in order, and choosing the right lender type, you can ensure a smooth loan approval process. Remember, your international education dream is within reach with smart financial planning.